Calculation of the economic effect from the introduction of an automation system. Calculation of the economic efficiency of the implemented IS Calculation of the economic efficiency of the implementation of the information system

Ministry of Education and Science Russian Federation

Federal Agency for Education

SEI HPE "Ivanovo State University"

Faculty of Economics

department information technologies in economics

and production organization

Economic evaluation of the effectiveness of information systems. Part 2

Methodical instructions for practical exercises

in the discipline "Efficiency of IS"

for students of the specialty

"Applied Informatics in Economics"

full-time and part-time education

Ivanovo State University Publishing House

Compilers: Candidate of Economic Sciences, Associate Professor I.V. Guskova,

Art. teacher A.V. Romanova

The guidelines provide the theoretical foundations of the discipline for analyzing the economic efficiency of implementing information systems, highlight the performance indicators of automated solutions and the features of their calculation, consider the classification of known methods and approaches for assessing the effect of implementing IT projects, and a list of recommended literature.

Methodological instructions are intended for practical training in the course "Efficiency of IS" and writing term papers and theses for students of the specialty "Applied Informatics in Economics" of all forms of education.

Printed by decision of the methodological commission

Faculty of Economics

Ivanovo State University

Reviewer: candidate of technical sciences, associate professor CM. Golyakov(IvGU)

|

1. Methods for evaluating the effectiveness of information systems | |

|

1.1.Traditional financial methods | |

|

1.1.1. Calculation of total cost of ownership (TCO) | |

|

1.2. Qualitative Methods | |

|

1.3. Probabilistic Methods | |

|

2. Indicators economic efficiency automated economic information systems (AEIS) | |

|

3. Indicators of direct and indirect efficiency of automated information | |

|

4. Methodology for assessing economic efficiency from the implementation of tasks | |

1. Methods for evaluating the effectiveness of information systems

When implementing a software product that supports the concept of a balanced scorecard, organizations want to spend a minimum of money and get the maximum benefit from its operation.

However, at present, the introduction of modern information technologies, even with a fairly wide offer in this market and regular price reductions, remains an expensive project. Therefore, the question of the need to assess the feasibility of introducing such systems becomes relevant. That is, the economic benefits from the implementation of IT projects can be realized if they are identified already in the design process and incorporated (directly or indirectly) into the project's targets. Project performance management is necessary, as the enterprise incurs large losses due to the irrational implementation of new IT technology. To assess the economic efficiency, a number of methods have been developed, which can be conditionally divided into three groups:

traditional financial methods involving the determination of indicators such as Net Present Value (NPV), economic attractiveness (Economic Value Added, EVA), total cost of ownership (Total Cost of Ownership, TCO), etc.;

qualitative assessment methods, the main of which are the Balanced Scorecard, information economics (Information Economics, IE), asset portfolio management (Portfolio Management), etc.;

probabilistic evaluation methods: fair option price (Real Options Valuation, ROV), applied information economics (Applied Information Economics, AIE) etc.

Each of the above groups has a number of advantages and disadvantages, a preferred area of application, a degree of constructiveness and the possibility of integrating into a development strategy.

1.1. Traditional financial methods

These methodologies use traditional financial calculations, taking into account the specifics of IT and the need to assess risk.

Skripov D.K., Ph.D.

JSC VTB Bank, Deputy Head of Service in DIT

graduate group MBA CIO-32A

RANEPA School of IT Management under the President of the Russian Federation

Gribanov S.P.

School of IT Management RANEPA under the President of the Russian Federation

When implementing any information system in a large enterprise, the question always arises of the appropriateness of the costs associated with its cost. It is very important to fully evaluate all planned costs, including the cost of licenses, the cost of services for the implementation / improvement of the system, and the cost of maintenance. Although for most projects it is not possible to reliably translate into monetary form image and other intangible assessments caused by the introduction of this information system, a detailed analysis of direct and indirect costs and incomes allows us to draw a reliable conclusion about the need for its implementation.

To assess the result of the implementation of an information system, economic efficiency can be defined as the difference between the total income from the use of an information system and the costs of an information system during its life cycle. But before the implementation of the system, future income cannot be determined exactly, it can only be estimated based on the practice of implementing similar systems. Therefore, in the beginning, they usually talk only about qualitative forecast indicators.

As in many large companies, JSC VTB Bank is simultaneously implementing a large number of both mutually influencing and unrelated projects. Projects, as steps in the process of implementing a long-term IT strategy, in addition to compliance with the bank's business strategy, are also evaluated by the economic efficiency of information systems being implemented or improved. Especially in connection with the fact that decisions on the implementation of projects go through a long chain of people in the branched structure of the Bank, and in the end are accepted collectively by the Banking Information Technology Committee, a single method is needed that is transparent for representatives of various departments, allowing to compare the cost of projects and take responsibility decision to implement them.

JSC VTB Bank is the parent company of the VTB Group. The state's share in the capital of VTB Bank is 60.9%. VTB Group is an international financial group providing a wide range of banking services. VTB Group consists of VTB Bank and its subsidiary credit and financial institutions. Subsidiary credit institutions carry out banking operations, subsidiary financial institutions provide securities market services, insurance services or other financial services. VTB Group today consists of more than 30 companies in more than 20 countries around the world. The Group's companies employ more than 90,000 people.

In accordance with the development strategy of the VTB banking group, the main activity is to increase shareholder value.

Modern banking activity is impossible without the use of advanced information technologies by credit institutions, which allows not only to improve the quality of banking services provided, but also to expand their list. As practice shows, the use modern technologies credit institutions provides a significant increase in the efficiency of their activities.

IT Strategy is integral part general development strategy of VTB Group and determines the direction of IT development in VTB Group.

The main goals of the IT strategy are:

- optimization of IT expenses of VTB Group;

- improving the quality and reliability of IT services;

- providing additional competitive advantages for business through information technology;

- preparation of IT for a possible merger of large Russian banks of the Group.

Building a corporate governance system by VTB Group is aimed at maximum use its advantages, growing share in target markets, increasing efficiency indicators and increasing the level of capitalization of the VTB Group.

Thus, in the competitive conditions of the modern market, which require constant addition and / or change of banking products, a fast, efficient and manageable system of knowledge transfer between the Bank's employees is very important. The problems of knowledge transfer are further increased for the banking group as a whole.

The Group's current distance learning system is fragmented and does not currently meet the Group's needs, as it does not reflect the matrix management system and existing Global Business Lines.

The Group does not have the opportunity for rapid and standardized training across the Global Business Lines, Support Lines and Product Verticals.

Thus, it is necessary to create an operational system for introducing and disseminating knowledge across business lines, support lines and product verticals (including new procedures, policies, reporting standards, service standards, and others). United centralized system training for VTB Group companies will allow:

- ensure control over the quality of training in the Group, including by completing courses and providing feedback

- create a common group system for managing knowledge and sharing best practices

- ensure a significant reduction in costs for full-time training (not only functional, but also skills) without loss in quality, as well as for maintaining existing portals in different companies of the group, purchasing similar and interchangeable electronic courses.

Currently, distance learning systems are used autonomously in almost half of the Group's companies. At the same time, some portals contain less than ten courses and are practically not used.

The unified learning portal of VTB Group will allow you to:

- create a single learning space for all VTB Group companies

- create a platform for the exchange of knowledge between the companies of the Group

- implement PR functions at the Group level

- ensure that all employees of the Group have access to courses on personal effectiveness, management, work with software, etc.

The introduction of automated distance learning systems saves the cost of training employees from 30% to 80% (see for example), mainly due to a reduction in travel expenses for employees and / or trainers. Also, distance learning systems allow training tens of thousands of employees in a short time (for example, familiarization with a new banking product in two weeks).

The existing training system used by VTB Bank does not meet the requirements of the business. The processes for implementing system change do not satisfy users and need to be redesigned.

Methods for assessing economic efficiency

Currently, the literature mainly considers two approaches for assessing the economic efficiency of implementing an information system. The first of these is to use static valuations, without taking into account the time value of money. The main indicator is Total Cost of Ownership(Total Cost of Ownership, TCO). The specificity of the indicator is that it takes into account only the expenditure part of the project. There is no universal mechanism for calculating the indicator, direct and indirect costs are taken into account different types depending on the item being valued. Initially, Gartner Group in 1987, and then Interpose, later acquired by Gartner Group, back in 1994, proposed an approach using comparisons with similar average costs depending on the profile of the enterprise, which practically turned this method into the industry standard for estimating the cost of ownership of an information system.

ITIL Service Strategy () distinguishes six main characteristics of costs, divided into three groups, so that any type of cost can be attributed to exactly one of the elements of each of these three groups:

- Basic or operating

- Direct and indirect

- Fixed and variable costs.

Only fixed costs can be depreciated. Depreciation is necessary because information systems can cost significant amounts and be designed for many years of use, and of course their cost is much higher than the income for the first year of use. In accordance with tax code In the Russian Federation, electronic computing equipment belongs to the second group of depreciable fixed assets with a depreciation period of 2 to 3 years.

The main articles for which evaluation takes place ():

- equipment costs (Equipment Cost Unit, ECU);

- software costs (Software Cost Unit, SCU);

- personnel costs (Organization Cost Unit, OCU);

- accommodation costs (Accommodation Cost Unit, ACU);

- transfer costs (Transfer Cost Unit, TCU) associated with goods and services provided by other departments, i.e. internal settlements between departments of the organization;

- Cost Accounting (CA) costs associated with the IT financial management process.

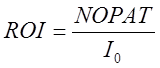

The next indicator for analyzing the implementation of the system is Return on investment(Return On Investment, ROI). This ratio shows the return on capital invested in the project:

,

(1)

where - invested funds, - cost at the end of the period, - profit. It is also called return on equity.

It is convenient to use the coefficient to answer the question of how effective the project is (). It is also closely related to the payback period of the project, this is the period of time that is needed for the project to break even.

Another useful indicator is Economic value added(Ecnomic Value Added, EVA). Economic value added is the difference between a company's net operating income and all costs incurred:

, (2)

where is the net operating profit after taxes,

– weighted average cost of capital, – invested funds.

The complexity of calculating the indicator is manifested in the evaluation of the parameters used.

If the return on investment is written as  ,

,

then the indicator of economic value added is defined as follows:

.

That is, any investment creates added value only if its return after taxes exceeds the weighted average cost of capital.

When it is not possible to explicitly assess the future profit, it is estimated by reducing the labor intensity or the absence of the need to perform operations due to the implementation of the information system. Estimates of the corresponding savings are multiplied by the average salary and increased by the amount of taxes (insurance contributions) and the cost of the workplace.

The key disadvantage of calculating TCO for evaluating economic efficiency is the lack of accounting for the revenue side of the project, as well as the change in the cost of money for long-term projects. Therefore, further we will use methods that take into account the concept of discounted cash flows with various modifications. Thus, for any cash flow, we will determine its value reduced to a given point in time.

The main indicator for this concept is the indicator net present value(Net Present Value, NPV):  (3)

(3)

where is the net present value, is the invested funds, r –

discount rate, is the total cash flow in k-th period, including financial, investment and operational flows. Typically, cash flows are recorded for periods of a year.

Another commonly used indicator is Internal rate of return(Internal Rate of Return, IRR). IRR is the rate at which Net Present Return becomes 0.

In order to calculate the Net present value, as well as for the value with which the Internal Rate of Return can be compared, it is necessary to estimate the discount rate as accurately as possible. The discount rate depends on the mechanisms for obtaining money for the project, as well as the ability to securely invest money. For a more accurate estimate or long term consideration of the economics of the project, the indicator of the Weighted Average Cost of Capital (WACC - WeightyAVerageCost ofCapital) , (4)

, (4)

where is the price of each source in the total cost of capital,

– tax rate, positive if expenses can be excluded from the taxable base, – rate of the corresponding source.

In practice, with a real assessment of the effectiveness of investment projects, in order to take responsibility investment decision, the above indicators are not calculated separately, but all together, since each of them has both positive and negative properties.

Thus, the following combination of methods is optimal from the point of view of completeness and minimization of the costs of the assessment:

- determination of the cost part of the project using the TCO method

- determination of the effects of the implementation of the system. this work may consist of several components:

- forecasting the effect of implementation based on the results achieved on previously successfully implemented similar projects in companies belonging to the same sector of the economy;

- forecasting the effect based on business customer assessments.

- taking into account the risks associated with the implementation project.

The existence of a corporate culture in a company often makes it difficult (and usually quite significant) to introduce new technologies, including new information systems. Therefore, corporate specifics must be taken into account.

An example of choosing an information system

In accordance with the IT strategy, the structure of the Bank, and taking into account the analysis of the market for automated learning systems, we will consider in detail the implementation of the Bank's requirements in the software products WebTutor by Websoft and Competentum Shareknowledge by Competentum. Widespread best of breed training systems for foreign companies, such as Saba or SAP R3, in addition to the severity of technical improvement, have the cost of only licenses that significantly exceeds the total cost of implementing and improving the Russian systems under consideration.

The weight of the scoring table criteria (see Fig. 1) was chosen based on the experience of implementing similar projects in the Bank. The main criterion is the cost (25%), since the project must be cost-effective. The next most important criterion (20%), and therefore with the greatest impact, is the compliance of the product as is with the stated business requirements. Since any rework carries some risk and also takes time, the system with the least required rework will of course have an advantage. The high weight of non-functional requirements (15%) is caused by the requirements of controlling internal divisions, such as the mandatory granting of access rights to information systems through a role structure. Modifications of information systems in order to fulfill such requirements, if they were not originally provided for in the design, usually require large time and material costs.

Rice. one . Evaluation of automated learning systems

The labor costs for the implementation project based on the Competentum Shareknowledge and Microsoft Sharepoint Server software product were estimated by Microsoft, the works received were converted into prices taking into account market prices large companies- automators. In accordance with the figures obtained, we calculate the financial indicators described above (the calculation is in millions of rubles):

TCO = 15

ROI = 19.6 / 15 - 1 = 30%

PI = 18.5 / 15 = 123%

NPV = 3.5

EVA = 4.6 - 0.035*3*15 = 3.03

IRR about 10%.

The main contribution to cost reduction is made by the expense item for transferring training standards to the Group's subsidiaries under the Change Management program. These costs include training for selected local providers and their certification for the program and for built-in elements, taking into account the average cost of payment to each of the providers, travel expenses, and quality control of trainings, that is, a trip to the affiliated bank of the provider-holder of the program and / or employees of the Corporate Training Service for support and quality control, as well as the very conduct of trainings by local providers in a subsidiary bank.

In the process of evaluating the economic efficiency, the following conclusions can be drawn:

Corporate management systems

Introduction

1. Analytical review

1.1 Goals and objectives of information systems

1.2 Classification of automated enterprise management systems

2. Goals and objectives

3. Main body

3.1 Characteristics of the enterprise

3.1.1 General information

3.1.2 Legal form

3.1.3 Main activity, services performed

3.1.4 Organizational structure management

3.2 Characteristics of the automated control system "HTControl"

3.2.1 Purpose

3.2.2 Organization of computational processes in the automated system "HTControl"

3.2.3 Selection and justification of an object for comparison: advantages, disadvantages

3.3 Calculation of the economic efficiency of the introduction of an automated system

3.3.1 Calculating the cost of building a system

3.3.2 Calculation of total cost savings

3.3.3 Calculation of capital investments and operating costs

3.3.4 Calculation of economic efficiency indicators and the expected annual economic effect from the implementation of the development

Work Conclusions

Bibliography

Introduction

Automated enterprise management systems are necessary to optimize and increase the efficiency of the work of managers and some other personnel departments of the enterprise. Experts say that managing an enterprise with the help of automated systems contributes to the growth of the competitiveness of any company. Automated enterprise management systems are especially important for managers. According to statistics, an ordinary manager spends about 60% of his precious time on reporting and compiling documentary tasks for staff. An effective database of employees, which is part of enterprise management, allows the manager to quickly access the necessary information and perform actions for the reception and movement of personnel. In addition to everything, enterprise management with the help of modern systems allows for automated payroll calculation based on many parameters. In particular, it provides for a position, individual benefits, sick leave, travel allowance, and more. The available information contributes to the prompt calculation and accounting of wage data in financial statements.

Today, automated enterprise management systems are offered by a great variety of foreign and domestic companies. The advantage of domestically produced products is their relatively low cost and adaptation to existing business principles. Foreign automated enterprise management systems have a higher price, however, as a rule, they offer the consumer the maximum saturation with various tools and functions.

1. Analytical review

.1 Goals and objectives of information systems

An enterprise is a single organism, and the improvement of one thing can lead to the slightest shift towards success in best case, or to a decrease in overall performance at worst. Managers, and especially finance managers, need to make complex decisions that affect the entire enterprise. And the workload of solving operational problems further complicates the management process.

To simplify the management of an enterprise, primarily financial, it is necessary to have an effective automated enterprise management system (AMS), which includes the functions of planning, management and analysis. What can the introduction of an automated enterprise management system give:

reduction of the total costs of the enterprise in the supply chain (when purchasing),

Increasing the speed of turnover

Reducing excess inventory to a minimum

increase and complexity of the product range,

improvement of product quality,

Completion of orders on time and improvement of the overall quality of customer service.

The automated control system performs technological functions for the accumulation, storage, transmission and processing of information. It develops, forms and functions in the regulations defined by the methods and structure of management activities adopted at a particular economic object, implements the goals and objectives facing it.

The main goals of automating the activities of the enterprise are:

· Collection, processing, analysis, storage and presentation of data on the activities of the organization and the external environment in a form convenient for making managerial decisions;

· Automation of business operations (technological operations) that make up the target activity of the enterprise;

· Automation of processes that ensure the implementation of core activities.

1.2 Classification of automated enterprise management systems

It is proposed to use the following classification of systems and subsystems of automated control systems. Depending on the level of service of production processes at the enterprise, the automated control system itself or its component (subsystems) can be assigned to different classes:

Class A: systems (subsystems) for managing technological objects and/or processes.

Class B: systems (subsystems) for the preparation and accounting of the production activities of the enterprise.

Class C: systems (subsystems) for planning and analyzing the production activities of an enterprise.

The first class A systems that were developed to solve process control problems mainly covered the scope of warehouse, accounting or material accounting. Their appearance is due to the fact that the accounting of materials (raw materials, finished products, goods) on the one hand is an eternal source of various problems for the management of the enterprise, and on the other hand (at a relatively large enterprise) one of the most labor-intensive areas that require constant attention. . The main "activity" of such a system is the accounting of materials.

These systems are typically characterized by the following properties:

· enough high level automation of performed functions;

the presence of an explicit function of control over the current state of the control object;

the presence of a feedback loop;

The objects of control and management of such a system are:

Technological equipment;

Sensors;

executive devices and mechanisms.

· a small time interval of data processing (i.e., the time interval between receiving data on the current state of the control object and issuing a control action on it);

· weak (insignificant) temporal dependence (correlation) between the dynamically changing states of control objects and the control system (subsystem).

As classic examples of class A systems can be considered: - Supervisory Control And Data Acquisition (supervisory control and data accumulation); - Distributed Control Systems (distributed control systems); Control - sequential control systems;

APCS - Automated control systems for technological processes.

The next stage in the improvement of material accounting was marked by planning systems for production or material (depending on the direction of the organization's activities) resources, they are classified as class B.

These systems, included in the standard, or rather two standards (MRP - Material Requirements Planning and MRP II - Manufacturing Requirements Planning), are very widespread in the West and have been successfully used by enterprises, primarily manufacturing industries, for a long time. The main principles that formed the basis of the MRP standard systems include:

description of production activity as a flow of interrelated orders;

Accounting for resource constraints when fulfilling orders;

minimization of production cycles and stocks;

Formation of supply and production orders based on sales orders and production schedules.

Of course, there are other functions of MRP: processing cycle planning, equipment loading planning, etc. It should be noted that the MRP standard systems solve the problem not so much of accounting as of managing the material resources of an enterprise.

Classic examples of class B systems can be considered: - Manufacturing Execution Systems (production management systems); - Material Requirements Planning (material requirements planning systems); II - Manufacturing Resource Planning (production resource planning systems); - C Resource Planning (production planning system); capacities); - Computing Aided Design (computer-aided design systems - CAD); - Computing Aided Manufacturing (automated production support systems); - Computing Aided Engineering (computer-aided engineering design systems - CAD); - Product Data Management (automated data management systems); - Customer Relationship Management (customer relationship management systems).

And all kinds accounting systems etc.

One of the reasons for the emergence of such systems is the need to identify individual management tasks at the level of the technological division of the enterprise.

Most popular on this moment a new type of information systems are systems of standard ERP - Enterprise Resource Planning. These are class C systems.

According to the APICS (American Production and Inventory Control Society) Dictionary, the term "ERP-system" (Enterprise Resource Planning - Enterprise Resource Management) can be used in two meanings. Firstly, it is an information system for identifying and planning all enterprise resources that are necessary for sales, production, purchases and accounting in the process of fulfilling customer orders. Secondly (in a more general context), it is a methodology for the effective planning and management of all enterprise resources that are necessary for the implementation of sales, production, procurement and accounting in the execution of customer orders in the areas of production, distribution and provision of services. - systems in their functionality cover not only warehouse accounting and material management, which is fully provided by the systems described above, but add to this all other resources of the enterprise, primarily cash. That is, ERP systems should cover all areas of the enterprise directly related to its activities. First of all, here we mean manufacturing enterprises. The systems of this standard support the implementation of the main financial and management functions.

The range of tasks solved by systems (subsystems) of this class can include:

planning of the enterprise activity;

regulation of global parameters of the enterprise;

planning and distribution of enterprise resources;

Preparation of production tasks and control of their execution.

the presence of interaction with the managing entity (staff) in the performance of their tasks;

interactivity of information processing.

The classic names of the class C system can be considered:

· ERP - Enterprise Resource Planning (Planning of Resources of the Enterprise);

· IRP - Intelligent Resource Planning (intellectual planning systems);

.2.1 Axapta

Microsoft Dynamics AX is a comprehensive ERP solution designed specifically for medium and large companies, which allows them to expand their capabilities and acquire new competitive advantages. Microsoft Axapta is ideal for companies looking for a fully integrated solution.

Benefits of Microsoft AxaptaAxapta is a system that:

allows you to conduct business exactly as you need;

improves interaction with customers, business partners and employees;

provides powerful, comprehensive functionality in a single integrated system;

Provides opportunities for rapid growth and business development.

Unity Axapta covers all areas of business, including manufacturing and distribution, supply chain and project management, financial management and business intelligence, customer relationship management and human resources.

The versatility of Microsoft Axapta

The system meets all the requirements of Russian and international standards accounting and legislation, can work in many languages and with different currencies.

Scalability

During the first installation of Microsoft Axapta, all system functions are installed. Functional unused features remain hidden from users and are activated when the appropriate license codes are entered into the system. When you purchase a system, you only pay for the features you intend to use, and if additional functionality is needed during operation, it can be "turned on" without resorting to complicated procedures for updating and integrating systems.

Work in several companies

Within a single installation of Microsoft Axapta, it is possible to maintain operational and financial accounting independently in several companies, while reducing the cost of maintaining and updating the system. This model of work is ideal for companies with several offices, branches or subsidiaries.

Customer and supplier files, the General Ledger chart of accounts, and other data can be either common to all companies or unique to each company, depending on the needs of the business. The system also supports trading operations between companies.

Microsoft Business Solutions-Axapta is based on the most advanced Western management technologies and high-tech solutions that allow you to effectively manage your enterprise. The system is more suitable for automating business processes within management accounting for medium and large enterprises in various fields economic activity.system is the core of your business, the basis that allows you to control the business processes of the enterprise. Axapta is an ERP system that works in an e-business environment. The uniqueness of the Axapta system lies in the fact that its modern technology provides a single enterprise information space, in which the back office and front office work as a single entity. Axapta offers a range of business intelligence capabilities to facilitate decision making and end-to-end customer relationship management (CRM).

The main modules of the Axapta system are:

finances;

trade and logistics;

· production;

· electronic commerce;

· personnel Management;

· projects;

customer relationship management (CRM - Customer Relationship Management);

knowledge management (KM - Knowledge Management);

supply chain management (SCM - Supply Chain Management) and others.

A wide range of functionality of the Axapta system allows you to get a number of specific advantages:

lower costs for the creation and support of the system;

ease of updating applications;

balance of redundant information;

Full integration of business processes.

The main blocks of the Axapta system are shown in Figure 1

Figure 1 - Parts of MS Axapta

automated saving investment expense

1.2.2 SAP R/3

The SAP R / 3 system consists of a set of application modules that support various business processes of the company and are integrated with each other in real time.

Finance (FI). The module is designed to organize the main financial statements, reporting on debtors, creditors and auxiliary accounting. It includes: General Ledger, Accounts Receivable, Accounts Payable, Financial Management, Special Ledger, Consolidation and Accounting Information System.

Controlling (CO). The module provides accounting for the costs and profits of the enterprise and includes: cost accounting at their places of origin (cost centers), cost accounting for orders, cost accounting for projects, costing, control of profitability (results), control of profit centers (profit centers) , accounting for production, controlling the activities of the enterprise.

Asset Management (AM). The module is designed to account for fixed assets and manage them. Key elements of the module: technical asset management, maintenance and repair of equipment, investment controlling and sale of assets, traditional asset accounting, asset replacement and depreciation, investment management.

Project management (PS). The PS application module supports the planning, management and monitoring of long-term projects with a high level of complexity. Key elements of the PS application module: financial and resource control, quality control, time management, project management information system, common modules.

Production planning (PP). The module is used to organize the planning and control of the production activities of the enterprise. Key elements of the application module: bill of materials (BOM), routings, work centers (locations), sales planning (SOP), production planning (MPS), material requirements planning (MRP), production control (SFC), production orders, costing per product, cost accounting by processes, mass production, planning of continuous production.

Materials management (MM). The module supports the supply and inventory management functions used in various business operations. Key elements: material purchasing, inventory management, warehouse management, invoice control, material inventory valuation, supplier qualification, work and service processing, purchasing information system and inventory management information system.

Sales (SD). The module solves distribution, sales, supply and billing tasks. Key elements: pre-sales support, inquiry processing, offer processing, order processing, delivery processing, invoicing (invoicing), sales information system.

Quality Management (QM). This module includes an information system and a quality management system. It provides support for quality planning, inspection and quality control in production and purchasing. Key elements: quality assurance, quality planning, quality management information system (QMIS).

Maintenance and repair of equipment (PM). The module helps to account for costs and plan resources for maintenance and repair. Key elements: unscheduled repairs, service management, preventive maintenance, specification maintenance, maintenance and repair information system.

Personnel management (HR). A fully integrated system for planning and managing the work of personnel. Key elements: personnel administration, payroll, time data management, travel expense calculation, benefits, recruitment of new employees, personnel planning and development, workforce utilization, seminar management, organizational management, personnel information system.

Information flow management (WF). This part of the system connects integrated application modules with common technologies, service tools and tools for all applications. Workflow management automates business processes in accordance with predefined procedures and rules. The module includes a multifunctional office system with built-in e-mail, a document management system, a universal classifier and a CAD integration system. When a certain event occurs, the corresponding process is started and the workflow manager initiates a workflow item. Data and documents are combined and processed at each step according to a certain logic.

Industry Solutions (IS). Combines SAP R/3 application modules and additional industry-specific functionality. Today there are industry solutions for industry: aviation and space, defense, automotive, oil and gas, chemical, pharmaceutical, engineering, consumer goods, electronics and non-manufacturing sectors: banks, insurance, government agencies, telecommunications, public utilities, healthcare, retail.

The diagram of the main blocks of SAP is shown in Figure 2.

Figure 2 - SAP main blocks

The base system serves as the basis of the SAP R/3 system and guarantees the integration of all application modules and independence from the hardware platform. The base system provides the ability to work in a multi-level distributed client-server architecture. The SAP R/3 system operates on UNIX, AS/400, Windows NT, S/390 servers and with various DBMS (Informix, Oracle, Microsoft SQL Server, DB2). Users can work on Windows, OSF/Motif, OS/2, or Macintosh.

It should be noted that only the main functions of the SAP R / 3 system are listed here and the extensive possibilities of working on the Internet / intranet are not mentioned, access external systems to SAP R/3 logic via BAPI (Business Application Programming Interface) interfaces, etc. R/3 is a configurable system

Even the most short review functions of the SAP R / 3 system shows its ability to solve the main tasks facing large organizations. SAP R/3 is the most comprehensive system to date. It is no coincidence that many leaders of the world economy have chosen it as the main enterprise management system. However, statistics show that more than a third of the companies that buy SAP R/3 are medium-sized firms with an annual turnover of less than $200 million. The thing is that SAP R/3 is a configurable system, therefore, having bought it, the enterprise will work with an individual version, configured exactly for its parameters. An indicator of the technical level of the system can be the way it is configured. The wider the possibilities of configuring and customizing the system without the need to rewrite it, the higher the technical level of this system. Therefore, the SAP R/3 parameter also occupies a leading position in the world.

The introduction of any financial and economic system pursues a very specific goal - increasing the efficiency of work and, ultimately, the survival of the enterprise in a competitive environment. To survive, an enterprise needs to move from traditional, function-oriented structures to more flexible, process-oriented forms. In practice, such a transition can be calculated and implemented only if the appropriate tools are available - for SAP R / 3 this is a specialized business engineering tool Business Engineer. With it, you can configure and customize the SAP R / 3 system so that it meets the needs of the enterprise, maintain this compliance throughout the entire life cycle of the system.

Business Engineering in SAP R/3

With the open standard Business-Engineer user interface, SAP partners and consultants can create pre-configured industry solutions based on SAP R/3 business scenarios. In addition, open interfaces enable SAP customers to develop their own templates for implementing the SAP R/3 system. Business-Engineer is included in the standard distribution of the SAP R/3 system and consists of three main components: SAP R/3 Business Configurator, which supports procedures for creating and maintaining enterprise models with automatic generation of appropriate tasks and customization profiles. The SAP R/3 reference model is an extensive SAP R/3 implementation metamodel, including an organizational model, a process model, a data model, a distribution model, and a business object model. The SAP R/3 Repository is the main data bank for the Reference Model, industry models, and generated enterprise models.

The system provides dynamic graphic modeling of business processes and can work in an interactive mode. The Business-Engineer tool greatly speeds up and simplifies the process of configuring an SAP R/3 system. When creating an enterprise model, typical business process scenarios supplied by SAP and its partners can be used. Business engineering tools can also be used to implement your own SAP R / 3 implementation methods, including using familiar dynamic business process modeling tools from other manufacturers.

1.2.3 Baan

BAAN is a Dutch company that develops enterprise management solutions for high-tech manufacturing and corporate logistics.

The main modules of the BAAN ERP system IV. - enterprise modeling: helps to reduce implementation time, reduce costs and accelerate return on investment. The subsystem is based on the unique tools of the implementation methodology called Orgware, developed based on the experience of implementing BAAN products in more than 50 countries around the world. The implementation process begins with a description or consideration of a reference model appropriate to the type and profile of the enterprise. At the next stage, the parameters of the business model are adjusted taking into account the requirements of the customer. Next, the system is configured and a menu is created for each specific user, the structure of which can include instructions and regulations , which determine the execution of individual tasks. At the end, an analysis of the enterprise's activities is carried out, on the basis of which solutions for the modernization of production are formed, further development directions are determined. The use of the system allows to reduce the implementation time to 3-10 months. - production: includes requirements planning, product configurator, project management, batch and order production management, supply chain management at the corporate production level. The "Production" subsystem is designed to work with all types of production management strategies. Moreover, the BAAN system has the flexibility to change the strategy during the life cycle of the project. The subsystem "Production" also provides the ability to change the location of the customer order anchor point (CODP), which determines the degree of influence of the customer order on the production cycle. The core of the "Production" subsystem is the "Main Production Schedule" (MPS) module. It is designed to help you with day-to-day production management as well as long-term planning and decision making. The subsystem allows you to implement all types of production environments and their combinations. - process: designed specifically for industries such as chemical, pharmaceutical, food and metallurgy, and supports the production process from research and development through production, procurement, sales, marketing and transportation. The subsystem works equally powerfully both within a separate enterprise and within a holding with geographically distributed enterprises. Subsystem BAAN - The process is fully integrated with all other subsystems BAAN. - Finance: is a management and financial accounting system for a company of any, the most complex organizational structure. The system of hierarchical links makes access to information and its processing more convenient, provides the greatest possible flexibility in structuring the necessary information. The multi-tier management structure allows you to analyze general ledger data, receivables and payables and other information, both at the level of an individual unit and at the level of the entire company. Three types of calendars are supported: financial, tax, reporting. Each calendar provides the ability to flexibly set the time frames of periods (quarter, month, week), which allows you to record daily transactions within one calendar and at the same time prepare data for taxation within another. The subsystem allows you to maintain documentation on different languages and carry out procedures for financial transactions with an unlimited number of currencies in the conditions of various countries: payment by checks (version of the USA and England), bills of exchange (France), bank orders, as well as by electronic means. The same financial operations are implemented for the conditions of the Russian Federation and other CIS countries. - sales, supply, warehouses: manages sales and purchases, contracts, inventories and storage, multi-level batch management and tracking the movement of batches. In addition, the module offers comprehensive management of external logistics and transportation, provides route optimization, transportation order management and support for transport work, support for general warehousing and packaging management. The subsystem "Sales, supply, warehouses" is designed to take care of the daily logistics of manufacturers and wholesalers. The subsystem is fully integrated with all products of the BAAN family, including "Production", "Project", "Service", "Transport" and "Finance", which provides your company with a comprehensive, accessible and unified management information system. This fully integrated procurement system includes electronic data interchange and communication with distribution requirements planning. - project: designed for procedures related to the development and execution of projects, as well as commercial offers to participate in tenders, and allows you to achieve high performance. BAAN - the project provides all stages of development and implementation of projects, as well as the preparation of contracts, including preliminary assessment of projects, contracting, budgeting, planning, project control, as well as warranty and post-warranty service. The system automatically generates purchase orders, production of products necessary for the implementation of projects, transportation, and has means of controlling payments. "BAAN - Project" is a powerful tool for controlling costs and revenues, a guarantee of meeting delivery deadlines. The use of "BAAN - Project" allows you to predict the impact of specific projects on the production potential and financial condition of the company, which makes it possible to increase productivity and make the best use of available resources. across all areas of the company. The form of data presentation allows for quick analysis to make error-free decisions. The "early warning system" built into the package allows you to make the necessary adjustments in a timely manner. - transport: created for companies involved in external logistics and transportation. Transportation companies, manufacturing and commercial companies, independently organizing their own transportation and logistics, will be able to rightfully appreciate the merits of the BAAN system. The package is designed for all types and modifications of transportation and has powerful modules for warehouse management common use and packaging. This unit can also be configured according to your company's requirements. Due to its flexibility, the "Transport" subsystem meets the most diverse needs of customers. - service: designed to organize the management of all types of services. It fully meets the requirements of after-sales and specialized service companies, as well as departments responsible for in-house service. The subsystem supports all types of maintenance: "periodic" (performing routine maintenance and carrying out preventive measures), "on call" (repair and troubleshooting in case of emergencies), and others, for example, commissioning service objects (installations). All data on equipment locations, customers, and maintenance and support contracts are available online and recorded for each component of the service object. All types of service can be performed taking into account warranty obligations.

The structure of the BAAN system is shown in Figure 3.

Figure 3 - Structure of the BAAN system

Based on the results of the calculations, it is also necessary to calculate the savings in labor intensity of work, savings in wages, savings in consumable materials, total savings for the implemented automated control system, capital investments of consumers, operating costs and the economic efficiency ratio.

3. Main body

.1 Characteristics of the enterprise

.1.1 General information

Company " High tech" has existed on the market of household and office equipment since 2002. The company is engaged in the transport logistics of household appliances and electronics. Transport logistics is a system for organizing delivery, namely, for moving any material objects from one point to another along the optimal route. LLC " High Technologies" was organized in Bryansk. At first, the company worked with several private stores household appliances located in the Bryansk region, supplying goods from suppliers in Moscow, renting a small warehouse where, before delivering the goods to customers, they were delivered from suppliers in Moscow. Later, routes were established and deliveries began to be carried out at their own expense, using the developed delivery schemes, which reduced the cost of goods for the client. By 2007, not only about half of the stores in the Bryansk region, but also some large shopping centers in Bryansk become clients of the company. The company already had a large warehouse, an office and an accounting department, where 3 loaders, a logistician, an accountant and two forwarders worked. Deliveries of goods began to be carried out regularly - 2 times a week. The range of suppliers has also expanded considerably. In 2010, a decision was made to establish a branch of the company in Kaluga. This decision was not taken by chance, as the company planned to work not only with clients in Kaluga and the Kaluga region, but also with clients located in the nearby regions: Tula, Oryol, Kursk. The reason for establishing a branch in Kaluga was that the Kaluga region is almost equidistant from neighboring regions and, from the point of view of transport logistics, is ideally suited for transportation to neighboring regions at minimal cost. Also, the main advantage of organizing a branch in this city was that here the company had practically no serious competitors. In Kaluga, a warehouse was rented and workers were hired, contracts with clients were also drawn up. Currently, the company uses a wide range of suppliers, offers consumers a wide range of goods at minimum prices, delivers goods at its own expense, using pre-designed delivery schemes. Deliveries of goods are carried out regularly in order to maximize the turnover. The company "High Technologies" seeks to quickly and flexibly solve the tasks assigned to it, and is open to proposals for working with business partners, cooperates with many wholesale and manufacturing organizations and offers various work schemes that are most convenient for partners. The company's policy is aimed at long-term and mutually beneficial cooperation with customers.

.1.2 Legal form

LLC "High Technologies" - a limited liability company (LLC) - is entity, established by one or more persons, the authorized capital of which is divided into certain shares (the amount of which is established by the constituent documents). Members of an LLC bear the risk of loss only to the extent of the value of their contributions. The constituent documents of the company are: the memorandum of association and the charter, which indicate the participants, the size of the authorized capital, the share of each participant, etc. Therefore, if one of the participants sells his share, this will inevitably entail changes in the charter of the company, with the mandatory registration of these changes in the bodies state power.

3.1.3 Main activity, services performed

The company "High Technologies" carries out wholesale and retail deliveries of electronics: computer equipment and components for it, large and small, household and office equipment, as well as telephones and other equipment most in demand on the market.

Services provided:

) Transportation of goods at your own expense;

) Unloading of goods directly to the client's premises;

) Delivery of warranty equipment to service centers;

) Control of information on the balance sheet of the client's enterprise, obtaining by the client of reliable information about the availability and price of goods.

.1.4 Organizational management structure

The organizational structure of management is shown in Figure 4.

Figure 4 - Organizational structure of the management of High Technologies LLC

Subordinate to the director is a senior manager, head of loading and chief accountant. The senior manager in turn supervises the firm's development manager and logistics specialist. Forwarders and loaders are subordinate to the head of loading. The assistant accountant reports to the chief accountant.

.2 Characteristics of the automated control system "HTControl"

.2.1 Purpose

When delivering goods to the company's warehouse, it is necessary to calculate the volume of goods that will be delivered to each client. The fact is that when calculating the volume of goods "manually", that is, simply on a sheet of paper by approximately adding the volume of each type of product, some inaccuracies are quite likely, which in the future may affect the company's image or even cause losses, in particular:

Overabundance of the calculation of the volume of goods.

When calculating the volume of goods came out to 14 cubic meters, based on this, a car with a capacity of 16 cubic meters was ordered. When loading goods into a truck, it may turn out that more than 16 cubic meters of goods have accumulated. In this case, you will have to leave a small part of the ordered goods, which simply could not fit in the car, in the warehouse until the next delivery. At the same time, the client may be dissatisfied with the fact that not all the ordered goods were delivered to him, or that they were not delivered on time.

Lack of calculation of the volume of goods.

Let's say that when calculating the volume of goods, it turned out 18 cubic meters, we had to order freight car with a capacity of 24 cubic meters. And during loading it turned out that the goods were much smaller, and the order could fit in a Gazelle with a capacity of 16 cubic meters. And since the delivery of goods will cost much more in a car with a larger capacity, firms will lose part of the profits. This automated system helps solve these problems. An automated system allows you to most accurately and quickly calculate the physical volume of goods for a specific client of the company (customer), which is usually a store. Also, this automated system can calculate the amount of money for which a certain order or group of orders was made, the physical volume of which must fit in a truck. This system can be used by managers of the firm, they add new product or remove goods from the price list, adjust the prices of goods. The system will help to accurately determine the amount of the ordered goods. It will also make it easier for accountants to keep track of goods. The most needed automated system will be the head of loading. It is he who must calculate with its help the volume of goods ordered by each client, so as not to make a mistake when choosing a truck.

.2.2 Organization of computational processes in the automated system "HTControl"

Managers of the company make a price list of goods using this automated system, adjust the prices of goods. The automated system consists of a product database and a user form for working with the database. The database is a price list of goods. For each product is assigned: code, name, short description, price per piece, and physical volume in cubic meters. The client, guided by the company's price list, forms an order, then sends it to managers. Managers verify it and approve it, then using an automated system, they calculate the order amount and transfer the documentation to the accounting department. After accepting orders from customers, the senior manager calculates the total amount of goods using the user interface. In the user form, a list of products is presented, from which he can select a group of products, then his specific model and quantity, and this product will be added to the customer's order. Thus, a customer order is formed, which is presented as a list of goods items. After the order is formed, the senior manager orders a truck with a suitable capacity. Then the truck is sent to the suppliers with a forwarder. Then the loaded car returns to the company's warehouse, the goods are unloaded and the goods are sorted by customers. The head of loading is engaged in the loading of goods, guided by the general list of ordered goods. When the sorting of goods is completed, the loading manager uses the system to calculate the volume of goods for each client. After the order is formed, the program calculates the physical volume of the goods and the cost of its order. Also, the system can offer one of the options for trucks, with the help of which the ordered goods can be delivered at minimal cost for its transportation. Then the head of loading directly orders trucks. The goods are shipped from the warehouse to trucks and then forwarders deliver the goods to customers.

.2.3 Selection and justification of an object for comparison: advantages, disadvantages

For small logistics companies, it is unprofitable to implement large solutions (BAAN, SAP). Therefore, the method of developing our own automated control system was chosen. Previously, the MS Excel software product was used to compile the price list of the company's goods. The calculation of the volume of the order was carried out manually, based on the experience of loading, which did not allow to accurately calculate the physical volume of the ordered goods.

3.3 Calculation of the economic efficiency of the introduction of an automated system

.3.1 Calculating the cost of building the system

The cost price is the sum of the development costs and the costs of maintaining and operating the equipment used in the implementation of the software product. The calculation of the cost of developing the program is made according to the formula (1).

![]() , (1)

, (1)

where C is the cost of the program, rubles; З р - developer's salary, rub. and deductions for social insurance, rub.; P e - the cost of operating the equipment, rub.; Н р - overhead costs (50% of the main wages developer), rub. The developer's salary is made up of the programmer's basic salary during the development of the program, additional salary, social security contributions and is calculated according to the formula.

![]() , (2)

, (2)

where Z o - the basic salary of a programmer during the development of the program, rub.; Z additional - additional wages, rub. (we will take 12% of the main one); About social - deductions for social insurance, rub. (26% of the amount of Z o and Z additional). The programmer's salary for the period of program development is calculated by the formula (3)

Where С h - salary for one hour of work of a specialist, rub.; T pr - the time spent on creating the program, hours; T pr can be technically justified and determined on the basis of regulatory documents or experimentally - statistically. Calculation of the cost of 1 hour of programmer's work is made according to the formula (4).

Where Z pm is the programmer's salary per month, (14,000 rubles); N - the number of working days in a month, days (22 days); 8 - duration of the working day, hour. Equipment operation costs are calculated by formula (5).

where C en - the cost of electricity, rub.; A o - the amount of depreciation during the development of the program, rub.; C rem - the cost of equipment repair, rub.; З op - wages of service personnel during the development of the program, (rub.) The cost of electricity is calculated by formula (6).

where M pr - electricity consumed by the computer, kWh; T m - computer time spent on creating the program, hour. (accept 50% of T pr); From kWh - the cost of one kWh, (2.28 rubles). The amount of depreciation for the period of development of the program is calculated by the linear method according to the formula (7).

![]() , (7)

, (7)

where N a is the annual depreciation rate, % is calculated using the formula (8);

C about - the cost of equipment, rub.; T n - standard service life, year; Ф d - the annual fund of the working time of the equipment, hour. It is determined by formula (9).

Fd \u003d ((365-S-V-Pr) x8-PPrx1) x S x (1-a / 100), (9)

where 365 is the number of calendar days in a year; C, B, Pr - the number of non-working days in a year: Saturdays, Sundays and holidays; 8 - shift duration, h; S is the number of equipment shifts per day; a is the percentage of time lost for equipment repair (take a = 3-5%) The cost of equipment repair for the period of program creation is determined by formula (10).

![]() , (10)

, (10)

Where H p is the amount of allocated funds for the repair of computer equipment relative to the cost of this equipment,% (take 2-4%); C about - the cost of equipment, rub. The salary of service personnel during the development of the program is calculated by the formula (11).

where Z op.o - the basic salary of maintenance personnel for the work performed, rub.; З op.dop - additional wages for service personnel, rub. (10% of the main); About social - deductions for social insurance, rub. (26% of the basic and additional wages) The basic wages of service personnel during the development of the program is determined by the formula (12).

![]() , (12)

, (12)

where n is the number of serviced PCs, pcs.;

З op.year - the annual salary of service personnel by categories of workers, rub. The complexity of the program can be determined either by standards or by expert estimates, that is, on the basis of experimental and statistical data of programmers, giving pessimistic, optimistic estimates. The expected duration of work is calculated by formula (13).

![]() , (13)

, (13)

Where T exp - used for the calculation of the complexity of the program Tpr, days; T opt and T pes are, respectively, the optimistic and pessimistic assessment of this program, days. The expected duration of work at the design stage is summarized in Table 1.

Table 1 - Expected duration of work at the design stage of the program

Name of works Duration of works (days) Minimum (T opt) Maximum (T pes) Expected 1. Development terms of reference 2. Analysis of terms of reference and data collection 3. Set the program on the PC * 4. Debugging a program on a PC * Note: an asterisk marks the work performed with the help of a computer. As a result of the calculation, 30 days were spent on the development of the program, of which 13.5 days were spent using a computer. Considering that the number of hours of work per day is 8, 240 hours were spent on the development of the program, of which 108 hours were the time of work on the computer. We summarize the data for calculating the cost of AIS in Table 2. Table 2 - Data for calculating the cost of the automated system "HTControl"

Index Values The complexity of creating a program The complexity of work on a PC Monthly salary of a software engineer Consumed energy Annual depreciation rate Cost of equipment Annual fund of equipment working time minus downtime for repairs Data on service personnel are given in table 3. Table 3 - Service personnel

The cost of 1 hour of programmer's work, calculated by formula (4), is: The basic salary of a programmer during the development of the program is calculated by the formula (3): Additional salary is 12% of W o: Social insurance contributions are 26% of the amount of Zo and Zdop: Thus, the salary of the developer, taking into account additional wages and social security contributions, is: The cost of electricity is calculated by the formula and is: The depreciation rate is calculated by the formula: The depreciation amount calculated by formula (7) is: The basic salary of service personnel during the development of the program is calculated by formula (12) and is: Additional salary is: Social security contributions are: Thus, the salary of service personnel during the creation of the program is calculated by formula (11) and is: Equipment operating costs are calculated by the formula and make up: Overhead costs are 50% of Zo: According to the results of the calculations, the cost of the program is: The total savings for the developed system can be calculated using the formula (14) where E S - total savings, rub.; E ZP - savings in wages, rubles; E MR - material savings, rub. Table 4 shows, for comparison, the duration of tasks solved manually and on a computer. Table 4 - Norms of work execution time

Index Symbol unit of measurement Basic option New option Annual labor intensity of data entry and correction operations man-hour Annual labor intensity of data search and processing operation man-hour Annual labor intensity of the operation for processing and outputting data man-hour Savings on wages are calculated by formula (15). where DT - time savings, hours; From 1h/i - the cost of 1 hour of the performer's work, rub. calculated by formula (16) Where ZP and - salary of the performer, rub. α - coefficient that takes into account social payments (1.26) Saving labor intensity of work is calculated by formula (17). Where T b is the annual complexity of solving the problem of the base case, hours; T n - the annual complexity of solving the problem of the new version, hours; Savings on wages (with a monthly salary of the loading manager of 16,000 rubles) will be: Consumables savings represents the paper savings for printed price lists. With the cost of one sheet of 0.15 rubles, the savings on paper for 300 printed price lists per year will be (with the cost of ten sheets of paper per price list) 450 rubles. The total savings for the developed system will be: The results of the calculations are summarized in Table 5. Table 5 - Summary table of calculated indicators in this paragraph

where K - capital investments in the system, rub.; K K - capital investments in the computer for which this program is intended, rub.; Ф d - useful annual fund of the operating time of this computer, minus downtime for repairs, hour / year; T MB - machine time used by the consumer for the tasks that he solves with the help of the system, machine hours / year (table 5); C - the cost of the system used, rub. The value of TME is calculated in paragraph 4.5 and is 176 hours, the cost of the developed system. C is calculated in clause 4.4 and amounts to 39,756.5 rubles. Capital investments in the computer for which the developed system is intended will amount to 25,000 rubles. The useful annual working time fund of this computer is 1860 hours/year, minus downtime for repairs. The capital investment of the consumer will be: The calculation of operating costs associated with the operation of the program is carried out according to the formula given in clause 3.3.1 (see formula (5)). Table 6 provides data for calculating operating costs. Table 6 - Data for calculating the costs associated with the operation of the program

Name Units Meaning The cost of one hour of work on a PC, C 1h/i Coefficient taking into account the additional salary, W D Payroll coefficient, W N Power consumed by the computer, M pr The cost of electrical energy, C 1kW / h The average number of hours of operation of the system per year, taking into account downtime in repairs, F d Labor intensity of work on a computer, T MW The salary of maintenance personnel during the operation of the program is calculated by the formula (19) Thus, the salary of service personnel is: The cost of equipment repair is calculated by formula (10) and is: The cost of electricity is calculated by formula (6) and is: The amount of depreciation in computer science, calculated by formula (7), is: Depreciation deductions from the program are calculated using the formula (20) where A P - depreciation deductions from the program, rub.; T C - service life of this program, T C = 5 years. Operating costs are The workplace is automated, so additional costs for the maintenance of buildings and premises are not required. The total costs, taking into account other costs (2% of the total operating costs) will be: Let's calculate the economic efficiency of using the program. The calculation is carried out according to the formula (21). where E F - actual savings, rub. The actual savings will be: 65005.63 The criterion for the effectiveness of the creation and implementation of applied software products is the expected annual economic effect received by the consumer of the program. The annual economic effect is calculated by formula (22). E G \u003d E F -E H K (22) where E G - annual savings, rub./syst. E N » 0.25 - normative coefficient of economic efficiency Thus, the expected annual economic effect is equal to: E G \u003d 26193.77-0.25 * 49617.75 \u003d 38598.21 rubles. The payback period for capital expenditures for the development and implementation of an automated system is determined by formula (23). where T ok is the payback period of the product, year. The payback period is: The estimated coefficient of economic efficiency of capital costs for the development and implementation of AIS is calculated by the formula (24): Thus, we can conclude that the activities for the creation and implementation of AIS are effective (E p = 0.77 > E n = 0.25) and will pay off within 2.02 years, while the annual economic effect will be 38598.21 rubles. Summary technical and economic indicators of the introduction of an automated information system are shown in Table 7. Table 7 - Summary technical and economic indicators of development

Index Unit measurements ABIS AKVT 1. Technical indicators Average system uptime System cost Capital investments Expected annual economic effect Economic efficiency ratio Payback period Automated control systems are very popular today in any industry. The use of such systems allows you to optimize the work of the enterprise and reduce the risks of errors and shortcomings that may arise during the control of production by the employees of the organization. Automated enterprise management systems allow: ) to neutralize errors and shortcomings when calculating the cost of a print order, when accounting for the income and expenses of the enterprise; ) optimize accounting for the costs of materials and labor resources; ) analyze the results of the company's work over various periods of time; ) reduce labor costs for accounting and reporting on the work of the enterprise, which ultimately has a positive effect on the profitability of production; ) protect access to information from competitors and unauthorized persons. The indisputable advantage of automated control systems is that they do not require any additional investments. Automated control systems are quite easily amenable to the necessary adjustments in accordance with the requirements of the enterprise's workflow. In this term paper an assessment of the economic efficiency of the introduction of the automated information system "HTControl" was made. The cost of developing a program is the sum of the development costs and the costs of maintaining and operating the equipment used in the implementation of the software product. According to the results of the calculations, the cost of the program is 47252.16. Saving labor intensity of work - 564 days. Savings on wages - 64,603.63 rubles. Saving consumable materials - 450 rubles. The total savings for the developed system will be 65,053.63 rubles. The consumer's capital investments will amount to 49,617.75 rubles. Operating costs amount to 38859.86 rubles per year. The coefficient of economic efficiency is 0.77. Based on the above calculations, it was concluded that the activities for the creation and implementation of an automated system are effective and will pay off within 1.3 years, while the annual economic effect will be 38,598.21 rubles. 1. Antonov A.V. System analysis. Methodology. Building a model: Proc. allowance. - Obnins: IATE, 2011. - 272 p. Volova V.N. Fundamentals of systems theory and system analysis / V.N. Volova, A.A. Denisov. - St. Petersburg: SPbGTU, 2010. - 510 p. Gasarov D.V. Intelligent information systems. - M.: Higher. sh., 2010. - 431 p. Ostreikovsky V.A. Automated information systems in the economy: Proc. allowance. - Wed t: SRGU, 2009. - 165 p. Ostreikovsky V.A. Modern information technologies for economists: Proc. allowance. Part 1. Introduction to automated information technology. - Wed t: SRGU, 2010. - 72 p. Automated Information Technologies in Economics / Ed. prof. G.A. Titorenko. - M.: Computer, UNITI, 2008. - 400 p. ACS on industrial enterprise: Methods of creation: Directory / S.B. Mikhalev, R.S. Sedenov, A.S. Grinber and others - M.: Energoatomizdat, 2009. M. Khokhlova, article "The modern market of enterprise management systems", Moscow University Press, 2007. - 256 p. Yu. Tokarev, article "Corporate information systems and a consortium of developers", - M .: Faculty of Economics, Moscow State University, TEIS 10.I.I. Karpachev, "Classification of computer systems for enterprise management", 2008. Professional business intelligence system [electronic resource] - Free access mode http://querycom.ru/company/2638916 12. Independent ERP-portal [electronic resource] - Access mode: //www.erp-online.ru free, Zagl. from the screen - Yaz.rus 13. Economic newspaper electronic resource] - Mode of access http://www.economics.ru free, Zagl. from the screen - Yaz.rus

![]()

![]()

![]()

![]()

.3.2 Calculation of total cost savings

![]() , (15)

, (15)

![]() (16)

(16)

3.3.3 Calculation of capital investments and operating costs

![]() , (18)

, (18)

![]()

![]()

![]()

3.3.4 Calculation of economic efficiency indicators and the expected annual economic effect from the implementation of the development

![]()

(24)

(24)![]()

Work Conclusions

Bibliography

When evaluating the effectiveness of creating a functioning CAD TP, the approaches described above are used. At the same time, the functioning of CAD TP gives specific indirect economic effect

| (13.6) |

where is the direct economic effect;

indirect economic effect. Let us introduce the following concepts:

The coefficient of comparative efficiency is determined by the formula

where is the annual cost savings.

Implementation information technologies is associated with capital investments both for the purchase of equipment and for the development of projects, the implementation preparatory work and staff training. Therefore, implementation should be preceded by economic justification for expediency implementation of information systems (IS). This means that the effectiveness of the application must be calculated. automated information technologies (AIT).

Under the effectiveness of automated information transformation is understood as the expediency of using computer and organizational technology in the formation, transmission and processing of data. Distinguish estimated and actual efficiency. Primary (calculated) is determined at the design stage of automation of information work, i.e., the development of a technical working project; the second (actual) - based on the results of the implementation of the technical working project.

The generalized criterion of economic efficiency is the minimum cost of living and materialized labor.